January 13, 2018 Marks the Start of a New Era in the Payment Industry

An Overview of the Status Quo of the Implementation of the PSD2 in Europe

Directive (EU) 2015/2366 of the European Parliament and of the Council of 25 November 2015 on payment services in the internal market, amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EC and Regulation (EU) No 1093/2010 and repealing Directive 2007/64/EC (“PSD2”) had to be transposed by the Member States by 13 January 2018. It replaces Directive 2007/64/EC of the European Parliament and of the Council of 13 November 2007 on payment services in the internal market, amending Directives 97/7/EC, 2002/65/EC, 2005/60/EC and 2006/48/EC and repealing Directive 97/5/EC (“PSD1”), which for the first time established a harmonised legal framework for non-cash payments in the internal market. The PSD2 aims to further develop the single European market for non-cash payments. Like PSD1, PSD2 also provides for full harmonisation: As a matter of principle, Member States are not allowed to maintain or introduce national legislation which deviates from the content of the Directive.

With the Act on the Implementation of the Second Payment Services Directive of 17 July 2017 (Zahlungsdiensteumsetzungsgestz (ZDUG) – BGBl. I p. 2446), Germany has transposed the PSD2 into national law. We have already reported on this.

Among our colleagues, we have asked what the situation is with regard to implementation in their countries. Specifically, we have asked our colleagues the following questions:

- How far is the implementation process of PSD 2 in your country?

- Can the directive be expected to be transposed in due course?

- Are there any specialties concerning the implementation?

With regard to question no. 3 we further asked to clarify the following:

- With regard to question no. 3 we further asked to clarify the following:From our point of view, it would be in particular interesting, whether there are specialities with regard to regulations of the PSD2, which the member states can implement, but do not have to (e.g. Art. 2 para. 5, Art. 8 paragraph 3, Art. 24 paragraph 3, Art. 29 para. 4, Art. 32 par. 1 and 4 , Art. 38 para. 2, Art. 42 para. 2, Art. 57 para. 3, Art. 58 para. 3, Art. 62 para. 2,3 and 5, Art. 63 para. 2 and 3, Art. 74 para. 1, Art. 76 para. 4, Art. 86, Art. 101 para. 2, Art. 109 para. 2 and 4).

- And also if there are uncertainties after the PSD2 has been implemented in your country. Just one example from Germany: “It is unclear whether AIS and PIS are obliged entities for purposes of Anti Money Laundering (AML) compliance. The German AML Act provides that all payment institutes are considered obliged entities with regard to AML-requirements (cf. Sec. 2 (1) Nr. 2 GwG). This would also include AIS and PIS (cf. Sec. 1 (1) No 1 ZDUG). However, the current AML law refers to a paragraph in the German payment law the numbering of which will not exist any longer after the PSD2 transposition law (ZDUG) takes effect. Therefore, the legislator will have to make some adjustments.”

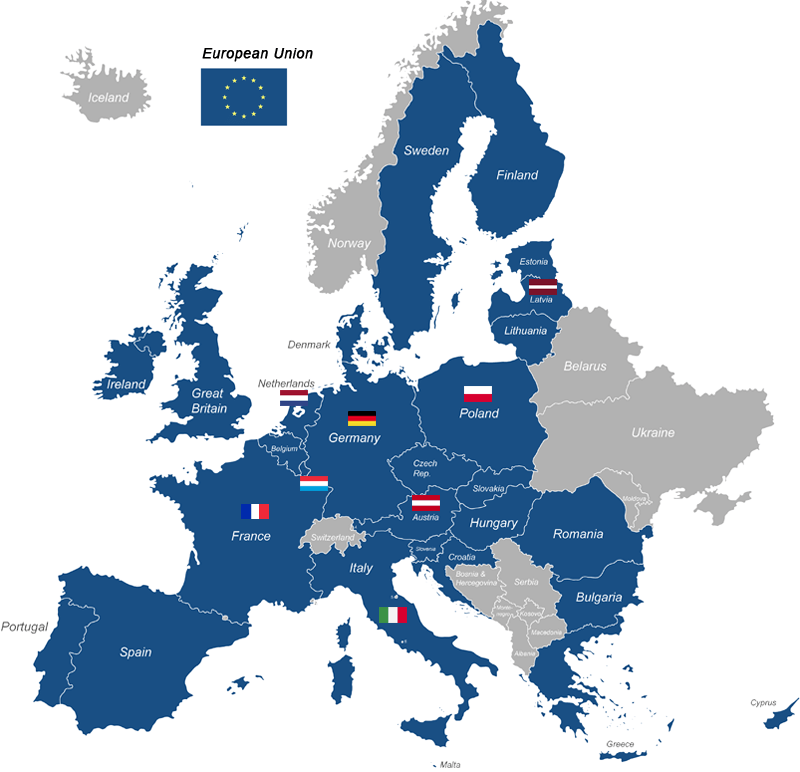

So far, colleagues from the following countries have replied: Austria, Italy, Latvia, Luxembourg, Poland and The Netherlands. We would like to express our sincere thanks to our colleagues (you can find the contact details under the respective country). In the coming weeks we will continue to supplement this EU map. If you have any questions about the PSD2, please check PayTechLaw or contact us. If you have any questions about the implementation of the PSD2, our colleagues in the respective countries will be happy to help you. The contact details can be found under the respective countries on the EU map.

For getting to know the status of the respective country, simply click on the corresponding flag on the EU map. Have fun discovering.

Germany

1. How far is the implementation process of PSD 2 in your country?

On 1st of June 2017, the German Bundestag passed the law implementing the Second Payment Services Directive (ZDUG) in the resolution version (Beschlussfassung) of the Finance Committee (Finanzausschuss). On 7 July 2017, the Bundesrat decided not to call on the Mediation Committee (Vermittlungsausschuss). The promulgation took place on 17 July 2017. The essential changes came into force on 13 January 2018.

2. Can the directive be expected to be transposed in due course?

The legislative changes took place in due course.

3. Are there any specific issues regarding the implementation?

It is unclear whether AIS and PIS are obliged entities for purposes of Anti Money Laundering (AML) compliance. The German AML Act provides that all payment institutes are considered obliged entities with regard to AML-requirements (cf. Sec. 2 (1) Nr. 2 GwG). This would also include AIS and PIS (cf. section 1 subsection 1 sentence 2 no. 7 and 8 ZAG). However, the current AML law refers to a paragraph in the German payment law the numbering of which does not exist any longer in the ZAG. Therefore, the legislator will have to make some adjustments.

BaFin also takes the PSD 2 as an opportunity to adapt existing administrative practices. On 29 November, BaFin published the long-awaited, newly amended guidance note on the German Payment Supervisory Act (PayTechLaw reported) and this guidance shows a few administrative changes, as for example:

The understanding of acquiring is now much broader and comprises more activities than it used to be under the former ZAG. Acquiring, which was called “payment authentication business” in the fomer ZAG, consisted mainly of the settlement of girocard or credit card transactions at POS. Now, acquiring is a payment service (named acquisition business) to process payment transactions which result in a transfer of funds and where the payment service provider has a contractual relationship with the payee to accept and process payment transactions (cf. section 1 subsection 35 ZAG). As a result BaFin will now treat businesses that provided payment transfer services („Finanztransfergeschäft“) under the former ZAG as acquisition businesses (PayTechLaw reported).

The exception for group of companies (the so called "Konzernprivileg") (cf. section 2 subsection 1 no. 13 ZAG) is now interpreted in a stricter way. Only payment transactions in which both the payer and the payee belong to the same group of companies are now covered by this exception. Payment transactions "entering" or "leaving the group of companies" are therefore not covered by this exception anymore. This means that the exception does not apply if the payer or payee (for example, the customer or the vendor) is not part of the group. (PayTechLaw reported).

Furthermore, the exception for agents (cf. section 2 subsection 1 no. 2 ZAG) is now applicable in fewer cases. BaFin sets out that this exemption applies where the agent acts on behalf of either the buyer or the seller. In addition, it is required that the agent has discretion to decide if and on which conditions a sale is concluded. Obviously, this will not be the case for many companies relying on this exception (PayTechLaw reported).

Also BaFin has put into more concrete terms the exceptions for payments made via payment instruments that are available only for the purchase of a limited range of products (cf. section 2 subsection 1 no. 10 b ZAG). The exception is only applicable, where the payment instrument is limited to the purchase of a fixed number of functionally related goods or services, as for example: fuel cards would be covered by the exception, provided that they only allow the purchase of vehicle-related goods and services which, in their functionality, are exclusively based on the premise "everything that moves the car".

If you have any further questions, please do not hesitate to contact Frank and/or Nasim.

Austria

1. How far is the implementation process of PSD2 in your country?

On 1 June 2018, the Payment Services Act 2018 (PSA 2018) entered into force. It implements PSD2 in Austria. It can be downloaded here. Link: https://www.ris.bka.gv.at/Dokumente/BgblAuth/BGBLA_2018_I_17/BGBLA_2018_I_17.html

2. Is the directive expected to be transposed into national law in due course?

No, see above.

3. Are there any specific issues regarding the implementation?

There are only a few specific issues:

- The existing Payment Services Act (PSA) will not be amended but repealed and substituted by the new PSA 2018.

- The PSA 2018 implements both the regulatory and the civil law provisions contained in PSD2.

In addition to question no. 3, there are certain provisions of PSD2, which the member states can implement, but do not have to. Austria uses this options as follows:

- Art. 2 para. 5 – Austria partly uses this option and exempts the Österreichische Kontrollbank AG from the application of the PSA 2018.

- Art. 8 para. 3 – Austria chooses to apply Art 9 PSD2 also to payment institutions which are included in the consolidated supervision of the parent credit institution pursuant to Directive 2013/36/EU.

- Art. 24 para. 3 – Austria uses this option.

- Art. 29 para. 4 – Austria makes use of this option and requires payment institutions operating in Austria through agents under the right of establishment, where their head office is situated in another member state, to appoint a central contact point in Austria.

- Art. 32 para. 1 and 4 – Austria does not use this option.

- Art. 38 para. 2 – Austria does not use this option (application of Title III to micro enterprises)

- Art. 42 para. 2 – Austria uses this option and increases the amounts for national law as follows: value payment transactions (to EUR 60 for individual payment transactions, EUR 300 for payment instruments with a respective spending limit and EUR 400 for prepaid payment instruments).

- Art. 57 para. 3 and Art. 58 para. 3 – Austria uses these options and requires PSPs to provide information on paper or another durable medium at least once a month. This is heavily criticized by the industry.

- Art. 61 para. 2 and 3 – Austria does not use this option.

- Art. 62 para. 5 – Austria uses this option and prohibits payees to require surcharges. The respective draft provision is disputed.

- Art. 63 para. 2 and 3 – Austria uses this option (see remark to Art. 42 para 2 PSD2 above).

- Art. 74 para. 1 – Austria uses this option.

- Art. 76 para. 4 – Austria does not use this option.

- Art. 86 – Austria does not use this option.

- Art. 101 para. 2 – Austria does not use this option.

- Art. 109 para. 2 and 4 – These two options are not used.

We would like to thank very much for the provided answers:

Bernd Fletzberger

PFR Rechtsanwälte

Nibelungengasse 11/4, 1010 Wien, Austria

Italy

1. How far is the implementation process of PSD2 in your country?

The Directive has been implemented through Legislative Decree No. 218 issued on December 15, 2017, published on the Official Gazette of the Republic of Italy on January 13, 2018, No. 10.

2. Is the directive expected to be transposed into national law in due course?

It is in force as of January 13, 2018 but with some exemptions for payment services and e-money institutions up to January 13, 2019.

3. Are there any specific issues regarding the implementation?

The Legislative Decree seeks to increase the level of transparency, competition and integration of the European payment card market by setting a limit on the interbank fees applied to payments made with payment cards: for debit card and prepaid card payments, the interbank fees for each payment transaction may not exceed 0.2% of the value of the transaction; for credit card transactions, the interbank commission per transaction may not exceed 0.3% of the value of the transaction. In addition, the Decree sets technical requirements and uniform marketing rules aiming to strengthen the harmonization of the sector and to ensure greater security, efficiency and competitiveness of electronic payments for the benefit of traders and consumers.

The Legislative Decree

(a) extends the rights of users of payment services, such as a reduced liability regime in the case of unauthorized payments, decreasing the maximum exemption for users from 150 to 50 euros, (b) promotes the use of electronic payment instruments,

(c) confirms and generalizes the ban on applying a surcharge for the use of a particular payment instrument.

With regard to interbank fees

• for "domestic transactions" carried out solely through payment cards, payment service providers will have to apply reduced fee commissions for payments of up to € 5 for all types of cards, compared to those applied to transactions of an equal or a higher amount, in order to promote the use of cards for these payments;

• for "domestic transactions" carried out through debit cards and as a transitional measure until December 2020, service providers may apply an interbank fee (i.e. from the card issuer to the acquirer) not exceeding the equivalent of 0.2% based on the annual average value of all domestic transactions carried out through debit cards within each payment card scheme.

In addition, there are better defined cases of what is excluded from the scope of the rules on payment services. According to the specific EU harmonized criteria of PSD2, this includes, for example, the following:

(i) the exclusion of "limited network" instruments due to the limited nature of the commercial networks in which they can be used, the very limited range of goods and services or specific social purposes, and

(ii) the possibility of using phone credit even for payment transactions made in the context of a charitable activity or for the purchase of tickets for services of a different nature (within the spending limit of 50 euros per single transaction and up to a maximum of 300 euros per month).

On the other hand, it seems that the measures concerning the Strong Customer Authentication and Secure Communication are expected to be implemented between April and July 2019.

As regards controls, the Legislative Decree stipulates that the national authorities responsible for ensuring compliance with the relevant provisions of the directive and the relevant regulation are the Bank of Italy and, for certain specific provisions, the Italian Antitrust Authority. Lastly, the amount of the applicable fines will be updated, distinguishing between those applicable to companies or entities and those applicable to individuals.

We would like to thank very much for the provided answers:

Fabrizio Colonna

STELE' PERELLI

Via L. Ariosto, 6 - 20145 Milano

Poland

1. How far is the implementation process of PSD2 in your country?

The PSD2’s implementation is still ongoing. The draft law adjusts national regulations, in particular the Act on Payment Services which is currently in force, to be in line with PSD2. The latest version of the draft law was adopted by the Polish government and submitted to the Polish parliament for plenary and parliamentary commission hearings. After adoption by both chambers of parliament, the law then needs to be signed by the President of the Republic of Poland and published in the Official Journal.

2. Is the directive expected to be transposed into national law in due course?

The transposition of the PSD2 is already belated and the law is expected to enter into force in c.a. March or April 2018.

3. Are there any specific issues regarding the implementation?

Polish implementation is going to provide for an additional grace period – those AIS and PIS providers active on the date of its entry into force will be able to continue their activities for a further 6 months without authorisation or registration. If PIS provider applies for authorisation or AIS provider applies for registration during this grace period, it will be entitled to provide its services on the same conditions as before the law entered into force, for the duration of the authorisation or registration procedure before the Polish FSA (but no longer than until the Commission Regulation on RTS on SC and SCA enters into force). A similar grace period has been introduced for other PIs to adjust to the PSD2 regulatory framework.

The draft law implementing PSD2 requires ASPSPs to use existing regulations regarding security of payments, which are accepted by the Polish FSA, until the entry into force of the Commission Regulation on RTS on SC and SCA. It is unclear whether it includes a prohibition on the sharing of credentials and technical measures aimed at preventing screen scraping.

The draft law will also introduce a new type of payment services providers – small payment institutions (SPIs). SPIs will be allowed to provide payment services, except for AIS & PIS, upon registration with the Polish FSA. The amount of payment transactions executed monthly by SPIs may not exceed € 1,500,000 (the average monthly amount in the most recent 12 months). A single user may not hold more than € 2,000 on the payment account. There are no planned requirements regarding SPIs’ own funds.

We would like to thank very much for the provided answers:

Michał Mostowik

dLK Legal

Ogrodowa City Gate, ul. Ogrodowa 58, 00-876 Warsaw, Poland

Latvia

1. How far is the implementation process of PSD2 in your country?

In Latvia, issues related to the provision of payment services are governed by the Law on Payment Services and Electronic Money (the “LPSEM”). The Financial and Capital Markets Commission (the “Commission”), which is the Latvian regulator in charge of overseeing the activities of, amongst others, payment service providers, has prepared draft amendments to the LPSEM aimed at transposing PSD2. Draft amendments to the LPSEM were circulated to the industry representatives (various associations and experts) for comments in mid-October 2017. Draft amendments are about to submitted for the vote to the Cabinet of Ministers (end of January 2018 / early February 2018). After approval by the Cabinet of Ministers, draft amendments will be submitted for the vote to the Parliament.

2. Is the directive expected to be transposed into national law in due course?

No. Because of the heavy workload of the Commission, the draft amendments to the LPSEM were prepared with some delay. Based on the current status of the draft amendments, one can expect PSD2 to be transposed into national law by February / March 2018 at the earliest.

3. Are there any specific issues regarding the implementation?

With respect to the majority of provisions of PSD2 which allow Member States to exercise certain discretionary powers, the existing LPSEM requirements will remain unchanged (i.e. identical to the ones established by transposing PSD1). The most extensive changes relate to the exemption regime (Article 32 PSD2), which might result in an obligation of a significant number of currently exempted service providers to obtain proper authorisation (see below for details).

Below is information on the options chosen by Latvian legislation with respect to the transposition of PSD2 to the extent such discretionary powers of member states were established by PSD2. Please note, however, that the information below is provided based on the draft amendments to the LPSEM as distributed by the Commission in mid-October 2017 and it might change up until the date of adoption of the respective amendments to the LPSEM.

Article 2(5) PSD2: Option chosen and institutions referred to in points (4) to (23) of Article 2(5) of Directive 2013/36/EU are exempted.

Article 8(3) PSD2: Option chosen – Article 9 requirements regarding own funds requirements not applied in relation to payment institutions which are included in the consolidated supervision of the parent credit institution.

Article 24(3) PSD2: Option chosen - requirements of Directive 2013/35/EU are applied.

Article 29(2) PSD2: The Commission will have a right to request information from the payment institutions having agents or branches in Latvia.

Article 29(4) PSD2: The Commission will have a right to request payment institutions operating in Latvia through agents to establish a central contact point in Latvia.

Article 32(1) PSD2: As the result of implementing PSD2, the regime allowing certain entities to provide payment services without undergoing a full-scale licensing process will be significantly revised. Thus, only companies who provide money remittance services will be allowed to operate without obtaining a license (previously only the service providers of payment transactions where funds were covered by a credit line could not benefit from the exemption). Furthermore, the users of the payment services will have to be in Latvia or will have to have a close link (personal/professional) to Latvia. Last but not least, the monthly average value of the payments shall not exceed 3 million euros (this requirement remains unchanged).

Article 32(4) PSD2: Option chosen – only authorised payment institutions may grant credit according to Article 18(4) of PSD2.

Article 38 PSD2: Option not chosen, Title III provisions are not applied with respect to micro enterprises in the same way as to consumers.

Article 42(2) PSD2: Option not chosen, limits of 30 euros and 150 euros apply.

Article 55(6) PSD2: Option to provide for more favourable provisions for payment service users not chosen.

Article 57(3) PSD2: Option to require payment service providers to provide information on paper or on another durable medium at least once a month, free of charge, not chosen.

Article 58(3) PSD2: Option to require payment service providers to provide information on paper or on another durable medium at least once a month, free of charge, not chosen.

Article 61(2) PSD2: Option to waive application of Article 102 PSD2 in case the payment service user is not a consumer is not chosen.

Article 61(3) PSD2: Option not chosen and Title IV is not applied with respect to micro enterprises in the same way as to consumers.

Article 62(5) PSD2: Option chosen – payee is not allowed to request charges with respect to the usage of the particular payment instrument.

Article 63(2) PSD2: Option not chosen – respective limits of 30 euros and 150 euros apply.

Article 63(3) PSD2: Latvia will not exercise the right to limit the derogation.

Article 74(1): The payer will have to bear the losses up to 50 euros relating to any unauthorised payment transaction.

Article 86 PSD2: Option to provide for shorter maximum execution times for national payment transactions is not chosen.

Article 101(2) PSD2: Option to introduce or maintain rules on dispute resolution procedures that are more advantageous to the payment service user is not chosen.

Article 109(2) PSD2: Option chosen – authorisation of the existing authorised payment institutions will remain in force.

Article 109(4) PSD2: Option not chosen - entities benefiting from the exemption will have to re-submit the necessary documentation to the Commission by 13 July 2018.

We would like to thank very much for the provided answers:

Zane Veidemane-Bērziņa

Kronbergs Čukste Derling

Muitas iela 1, LV-1010, Riga, Latvia

The Netherlands

1. How far is the implementation process of PSD2 in your country?

The draft Dutch PSD2 Implementation Act and the draft explanatory notes were published on 18 November 2016. The consultation period ended 15 December 2016.

The proposal for the Dutch PSD2 Implementation Act plus explanatory notes were presented to the Dutch Parliament in October 2017. Thereafter, a hearing took place of the Finance Commission of the Parliament that lead to a report with about 140 questions. The Dutch Ministry of Finance is expected to respond to those questions soon. Thereafter, further discussions in Parliament may be expected. Approval by the Senate is also required (but this should in principle be a formality).

2. Can the directive be expected to be transposed in due course?

June 2018 is the latest estimate.

3. Are there any specific issues concerning the implementation?

Scope of PSD2 - authorisation requirement

According to the Dutch Financial Supervision Act (DFSA), payment service providers only need authorisation if it is their business to provide payment services. The Dutch Central Bank (DNB) currently takes the position that this means that the service must be separately identifiable and not merely auxiliary to a principal activity not qualifying as a payment service.

The explanatory notes state that an authorisation will be required if payment services are rendered in the performance of a regular occupation or business activity. The explanatory notes further explain that, due to implementation working groups in Brussels it is assumed that it is no longer relevant whether or not the payment service is the principal activity.

Guidance from DNB on PSD2 can be found on http://www.toezicht.dnb.nl/4/1/50-236570.jsp (Dutch only).

There is also a specific Q&A on e-commerce platforms. See http://www.toezicht.dnb.nl/3/50-236584.jsp (Dutch only).

PSD2 license applications cannot be formally submitted yet to DNB. DNB however made available a draft application form and explanatory notes to the form. See http://www.toezicht.dnb.nl/en/2/51-235603.jsp (also English).

DNB also lists the success factors for a license application. See http://www.toezicht.dnb.nl/en/2/51-235609.jsp. One of the DNB advices is to consult a legal adviser. DNB explicitly mentions that practice has shown that applications are often more complete and of a substantially higher quality if the applicant has sought advice, for example from a legal expert or an auditor who specialises in Dutch regulatory laws. DNB can assess a complete and well-founded application more quickly and more thoroughly.

Below is information on the options chosen by Dutch legislation with respect to the transposition of PSD2 to the extent such discretionary powers of member states were established by PSD2. Please note, however, that the information below is provided based on the proposal for the Dutch PSD2 Implementation Act and the explanatory notes thereto.

Article 2(5) PSD2: Option not chosen.

Article 8(3) PSD2: Option not chosen

Article 9 (1) and (3) PSD2: Options chosen

Article 24(3) PSD2: Option chosen

Article 29(2) PSD2: Option chosen

Article 29(4) PSD2: Option chosen

Article 32(1) PSD2: Option chosen (in accordance with the current regime)

Article 32(4) PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 38 (2) PSD2: Option not chosen. The Netherlands, after consultation with stakeholders, decided to not used this option, because it is insufficiently offers added value.

Article 42(2) PSD2: Option chosen

Article 55(6) PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 57(3) PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 58(3) PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 61(2) PSD2: Option chosen (in accordance with current regime).

Article 61(3) PSD2: Option not chosen. The Netherlands, after consultation with stakeholders, decided to not used this option, because it is insufficiently offers added value.

Article 62(5) PSD2: Option not chosen – payee is allowed to request charges with respect to the usage of the particular payment instrument (unless PSD2 provides for otherwise).

Article 63(2) PSD2: Option chosen (in accordance with current regime).

Article 63(3) PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 74(1): Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 86 PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 101(2) PSD2: Option not chosen. According to the explanatory notes there have not been shown a need for this.

Article 109(2) PSD2: Option chosen – authorisation of the existing authorised payment institutions will remain in force.

Article 109(4) PSD2: Option chosen

Data protection - Regulatory competence

Interestingly, the explanatory notes state that DNB monitors the PSD2 rules on data protection contained in PSD2 when granting authorisations and in its ongoing supervision. DNB as financial supervisor apparently should also supervise compliance with the data protection rules included in the DFSA pursuant to PSD2.

The Dutch Data Protection Authority (Dutch DPA) however recently claimed authority in relation to 94 PSD2. The discussion on privacy and the competent authority might further delay the implementation process.

AML/CFT and AISP/PISP?

An obliged entity is, according to the Dutch AML/CFT Act, amongst others, a payment service provider as defined in the Dutch Financial Supervision Act. A payment service provider is anyone who renders payment services in the course of their business. Payment services are defined as those activities mentioned in the annex to the PSD, which – once the PSD2 is implemented – means the PSD2.

We would like to thank very much for the provided answers:

Arno Voerman

Van Doorne

Jachthavenweg 121, 1081 KM Amsterdam, The Netherlands

Luxembourg

1. How far is the implementation process of PSD2 in your country?

PSD2 has been transposed in Luxembourg by the law of 20 July 2018, which can be found here.

2. Can the directive be expected to be transposed in due course?

No, see above.

3. Are there any specific issues concerning the implementation?

The existing legal framework i.e. the law of 10 November 2009 on payment services (LPS) is extensively amended with the implementation of PSD2. The options chosen by Luxembourg in the framework of the discretionary powers granted to the member states by PSD2 with respect to its transposition are listed here below:

Article 2(5) PSD2: Option not chosen

Article 8(3) PSD2: Option chosen – new Article 16(4) LPS

Article 24(3) PSD2: Option chosen – new Article 33(2) LPS

Article 29(4) PSD2: Option chosen – new Article 34(6bis) section 2 LPS

Article 32(1) PSD2: Option chosen – new Article 48(1) LPS

Article 32(4) PSD2: Option chosen - new Article 48(2) LPS

Article 38(2) PSD2: Option not chosen

Article 42(2) PSD2: Option chosen - new Article 63(2) LPS

Article 57(3) PSD2: Option not chosen

Article 58(3) PSD2: Option not chosen

Article 62(2), (3), (5) PSD2: Option chosen – new Article 79(3) LPS

Article 63(2) PSD2: Option chosen - new Article 80(2) LPS

Article 63(3) PSD2: Option not chosen

Article 74(1) PSD2: Option not chosen

Article 76(4) PSD2: Option not chosen

Article 86 PSD2: Option not chosen

Article 101(2) PSD2: Option not chosen

Article 109(2) PSD2: Option chosen - new Article 116 LPS

Article 109(4) PSD2: Option chosen - new Article 116 LPS

-

Potential uncertainties in the implementation of PSD2 have not shown up so far.

We would like to thank very much for the provided answers:

Charles Krier

Wildgen S.A.

69, Bd. de la Pétrusse, 2320 Luxembourg

France

1. How far is the implementation process of PSD2 in your country?

The Ordinance N°2017-1252 implementing PSD2 was published on 10 August 2017 and directly amends the relevant legal provisions of the French Monetary and Financial Code ("MFC").

The Ordinance has been completed by two decrees dated 31 August 2017 and five ministerial orders (“arrêtés”) dated 2 September, which finalize the implementation of PSD2 and, in particular, amend regulatory provisions of the MFC.

2. Is the directive be expected to be transposed in due course?

The Ordinance and the Decrees entered into force on 13 January 2018.

3. Are there any specific issues regarding the implementation?

France implemented several optional provisions of PSD2, specifically the following:

Art. 29 para. 4: The central point of contact, set by the PSD 2 and, before, by by the 4th AML directive, seems to derive from a French initiative. Indeed, before AML4 and PSD 2, France legislation already required payment or electronic money institutions operating in France through agents or distributors to appoint a “permanent representative” in France.

The “permanent representative” will be replaced by the central contact point, in principle upon publication of the related Regulatory Technical Standards.

Art. 62 para.3: The article L.112-11 of the MFC already provided that the payment services provider could not prevent the payee requesting a charge from the payer or offering him a reduction. Any stipulation contrary to this principle is deemed unwritten.

Article 1 (1) of the Ordinance N°2017-1252, however, amended article L. 112-11 to comply in all respects with article 62.3 of the PSD2, by adding, (i) that the service providers cannot prevent the payee to steer the payer towards the use of a given payment instrument and (ii) that any charges applied shall not exceed the direct costs borne by the payee for the use of the specific payment instrument.

Art.62 para. 5: Despite the above, according to article L.112-12 of the MFC, the payee is not allowed to request charges with respect to the use of a particular payment instrument. Exceptions can be made to this prohibition only under conditions defined by decree, taken after the opinion of the French Competition Authority, considering the need to encourage competition and promote the use of efficient payment instruments.

Art.101 para. 2: Article L. 133-45 of the MFC reproduced the provisions of art. 99 and 101 concerning the complaint resolution procedures and information of the payment services users about the existence of ADR entity which is competent to deal with disputes concerning the rights and obligations of payment services providers.

France also implemented the following options:

- Article 2(5)

- Article 8(3)

- Article 24(3)

- Article 32(1) and (4)

- Article 57(3)

- Article 58(3)

- Article 74(1)

- Article 86

- Article 109(2) and (4)

- Article 109(4)

We would like to thank very much for the provided answers:

Benjamin May and David Roche

Aramis Société d’Avocats

9 rue Scribe, 75009 Paris, France